Stablecoins are no longer a niche digital asset experiment – they’ve matured into a cornerstone of global payments infrastructure. In 2025, stablecoins facilitated trillions of dollars in transactions, increasingly rivalling traditional payment networks in settlement value. What began as a crypto-native innovation has evolved into a mainstream financial tool used for payroll, treasury management, cross-border trade, and settlement between institutions.

But for most small and medium-sized enterprises (SMEs), the question is not whether stablecoins are innovative. The question is:

Can they operate seamlessly within everyday banking systems?

The Shift: From Speculation to Infrastructure

Stablecoins such as USDC, USDT, and PYUSD are dollar-backed digital tokens that move across blockchain networks. Unlike volatile cryptocurrencies, they are designed to maintain price stability relative to the U.S. dollar, making them suitable for real-world settlement.

Their advantages are increasingly evident:

- Near real-time settlement

- 24/7 availability

- Transparent transaction records

- Reduced reliance on correspondent banking chains

- Lower friction in cross-border payments

Despite these benefits, adoption has historically been limited by operational complexity.

For many organizations, especially SMEs unfamiliar with digital asset infrastructure, using stablecoins requires managing wallets, safeguarding private keys, maintaining exchange accounts, and reconciling across separate custody systems. Beyond operational friction, there were also legitimate governance questions around sanctions exposure, transaction monitoring, and regulatory oversight.

The technology showed promise. What it lacked was regulated integration.

FV Bank’s Approach: Integration with Governance

At FV Bank, the approach has been fundamentally different. Rather than asking businesses to adapt to crypto-native workflows, FV Bank integrated stablecoins directly into the banking layer.

The integration began with USDC in 2022, well ahead of the recent surge in institutional adoption, followed by USDT in 2024 and PYUSD in 2025. This phased expansion reflected growing client demand for regulated access to multiple dollar-backed stablecoin rails.

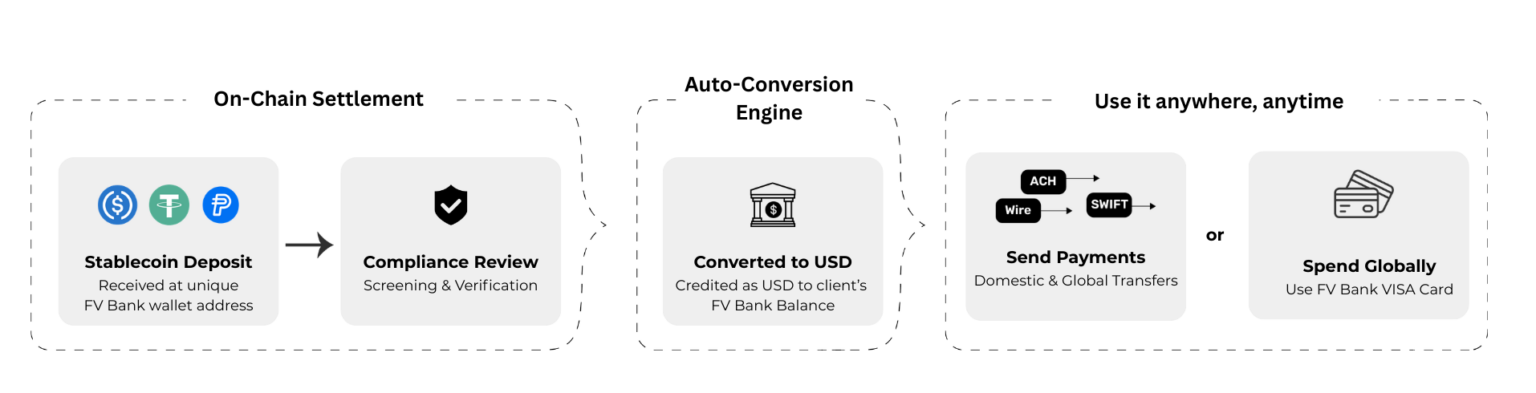

Each customer, whether business or individual, is assigned dedicated wallet addresses for supported stablecoins, directly linked to their bank account. Through the deposit interface, clients can generate an address or QR code to share with counterparties.

When stablecoins are received, they move through FV Bank’s standard transaction review processes, the same disciplined controls applied across all banking activities, before being automatically converted to USD and credited to the customer’s bank balance.

There is no requirement to manage private keys. No need for a separate exchange account. No parallel custody workflow.

From the customer’s perspective, funds simply arrive as USD inside a regulated bank account. The blockchain infrastructure operates in the background, delivering speed and transparency without introducing operational friction.

Spending Stablecoins Like Traditional Dollars

Integration extends beyond deposits.

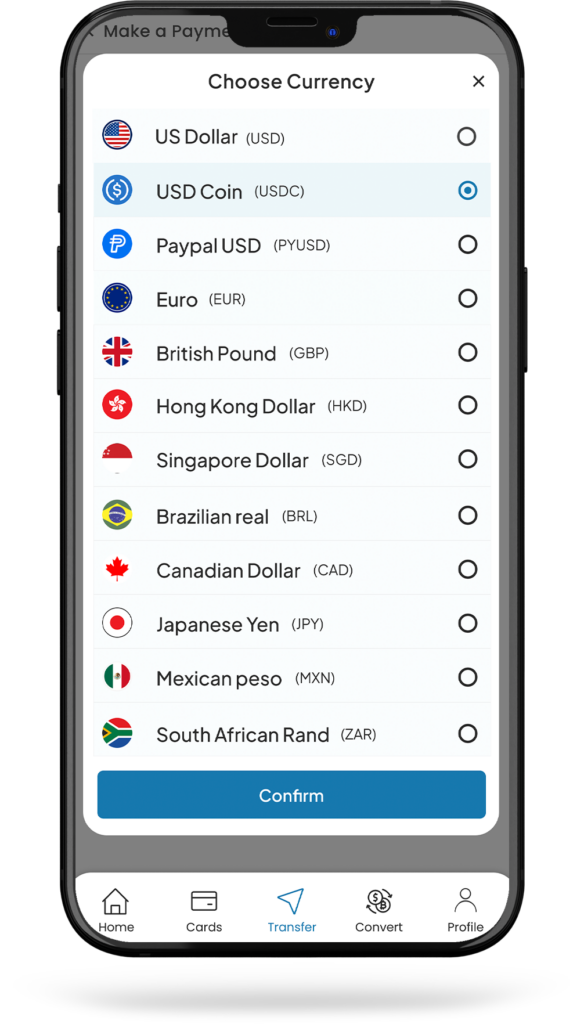

Once converted, funds function like any other USD balance within the account. Customers can initiate ACH transfers, send domestic and international wires, execute cross-border payments in multiple foreign currencies, or use their FV Bank VISA Debit Card for global spending.

Stablecoin deposits effectively become working capital.

Funds can be used for vendor payments, payroll, travel expenses, software subscriptions, cash withdrawals, or any transaction accepted by VISA worldwide, without additional conversion steps or delays.

Importantly, the model is fully bi-directional.

Conversely, customers can initiate stablecoin payments directly from their USD balance. When a stablecoin transfer is selected, the required USD amount is automatically converted into the chosen stablecoin and transferred to the beneficiary’s wallet address.

This architecture enables seamless movement across different stablecoins within the same account.

For example, a USDT deposit is automatically converted into USD and credited to the customer’s bank account. That same balance can then be used to initiate outbound stablecoin payments in USDC or PYUSD, without requiring separate conversions or external platforms.

This built-in on-ramp and off-ramp allows businesses to move seamlessly between traditional banking rails and blockchain networks within a single regulated account.

A company can:

- Receive funds via stablecoin

- Pay domestic and international expenses through ACH, wire transfer or SWIFT

- Settle with a digital asset-native counterparty using stablecoins

- Manage operational spend globally through its VISA debit card

All without leaving the banking environment.

Modern Infrastructure, Simplified

By combining traditional payment rails (ACH, Fedwire, SWIFT), stablecoin settlement (USDC, USDT, PYUSD), card issuance, and embedded governance controls within one integrated platform, FV Bank eliminates the fragmentation that historically limited adoption.

Stablecoins no longer require specialized systems or separate oversight. They become an extension of regulated banking infrastructure.

For modern SMEs and globally operating businesses, the advantages are practical:

- Faster settlement when speed matters

- Familiar banking controls where governance matters

- Flexible liquidity deployment across rails

For today’s SMEs and globally operating businesses, stablecoins are less about crypto exposure and more about practical outcomes – faster settlement, better liquidity control, and the ability to move capital across borders within a regulated banking environment.

That is what Banking the Future looks like in practice.

Frequently Asked Questions (FAQs)

What are stablecoins and how are they used in business payments?

Stablecoins are digital assets pegged to fiat currencies like the US dollar. Businesses use them for faster cross-border payments, payroll, treasury management, and settlement due to their stability and near real-time transfer capabilities.

How does FV Bank convert stablecoins into USD?

When a customer receives stablecoins such as USDC, USDT, or PYUSD, FV Bank processes the transaction through compliance checks and automatically converts the funds into USD, which is credited to the customer’s bank account.

Can businesses send stablecoin payments directly from their bank account?

Yes. Businesses can initiate stablecoin payments directly from their USD balance. The bank converts USD into the selected stablecoin and transfers it on-chain to the recipient’s wallet.

Do businesses need crypto wallets or exchanges to use stablecoins with FV Bank?

No. FV Bank integrates stablecoin functionality directly into the banking platform, eliminating the need for external wallets, private key management, or exchange accounts.

Can I convert between different stablecoins like USDT, USDC, and PYUSD?

Yes. For example, a USDT deposit is converted into USD and credited to your account. That same USD balance can be used to send payments in USDC or PYUSD without requiring additional conversions or external platforms.

Are stablecoin transactions secure and compliant?

Stablecoin transactions at FV Bank are subject to standard banking compliance controls, including transaction monitoring, sanctions screening, and audit processes, ensuring secure and regulated operations.

What are the benefits of using stablecoins for cross-border payments?

Stablecoins enable faster settlement, lower transaction friction, 24/7 availability, and reduced reliance on traditional correspondent banking networks.

Can stablecoins be used for everyday business expenses?

Yes. Once converted to USD, funds can be used for payroll, vendor payments, international transfers, and card-based spending globally.